At the 2025 Indonesia Mining Conference & Critical Metals Conference - Nickel-Cobalt-NEV Venue, Thomas Feng, Head of SMM's Nickel Industry Research, shared insights on "The Future Outlook of the Global Nickel Industry." He stated that throughout 2025, the supply-demand dynamics of Indonesia's nickel ore are expected to tighten, with overall prices anticipated to remain high. In the primary nickel market, SMM predicts that in the short term, influenced by factors such as policies, global nickel supply will tighten, maintaining a tight balance between supply and demand. However, in the long term, the primary nickel market is still expected to face a surplus. On the consumption side, the stainless steel industry will remain the primary downstream consumer sector in the nickel market, holding an unshakable position in nickel consumption.

Impact of Indonesia's Policy Changes on the Nickel Market in 2025

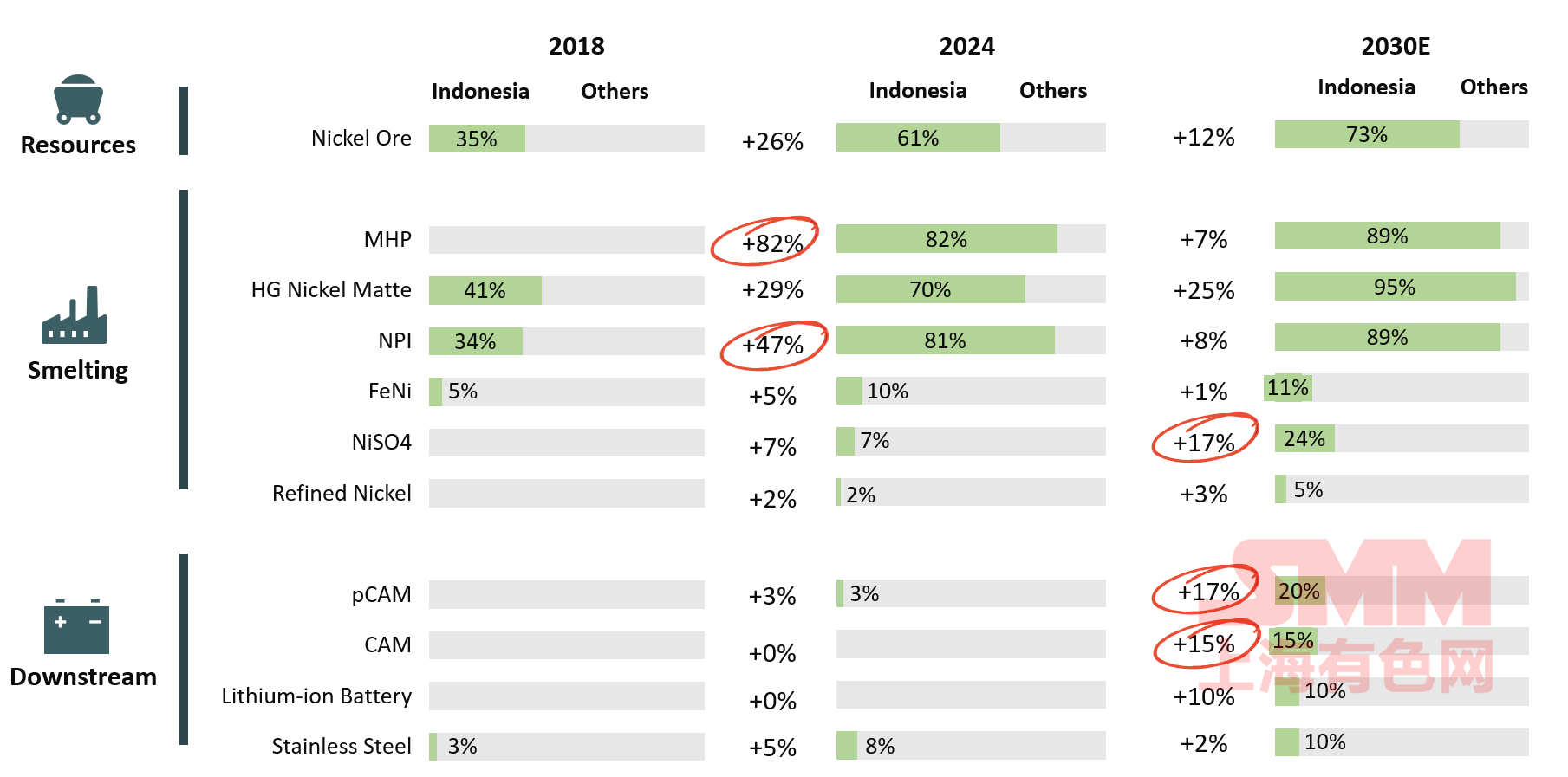

The proportion of various nickel products in Indonesia continues to rise

Indonesia possesses the world's richest nickel resource reserves and is a major supply source. This proportion is expected to increase further in the future.

As seen from the chart, from 2018 to 2024, the supply of nickel ore in Indonesia, from mining to smelting, has grown rapidly with the release of new capacities. For example, the intermediate product MHP had no production in 2018, but by 2024, its global supply share will reach 82%. In the NPI sector, Chinese companies have led the construction of numerous NPI plants using the RKEF process, significantly increasing Indonesia's NPI production. It rapidly escalated from a level of several hundred thousand tons to becoming the world's largest NPI producer, with its production accounting for 81% of the global total in 2024. Meanwhile, the supply share of other nickel products is also growing rapidly.

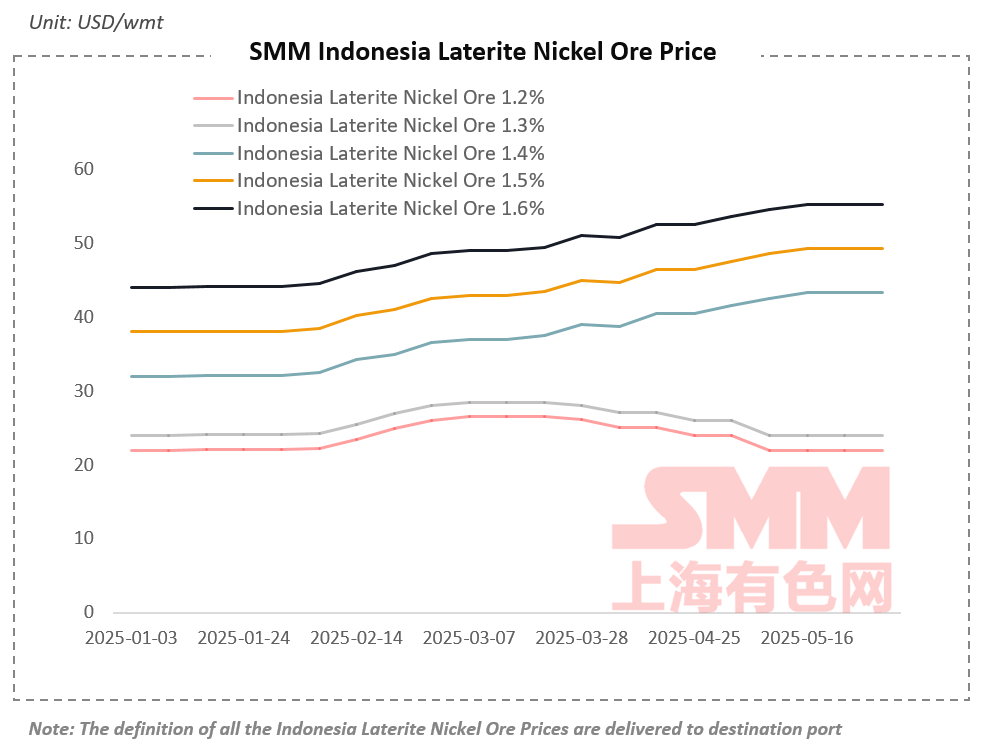

Since 2025, despite the supply surplus in the nickel market, nickel ore prices have been rising

To ensure the sustainability of nickel industry supply and increase government-related tax revenues, a series of nickel-related policies have been introduced, including RKAB, SIMBARA, and HMA. RKAB is a key policy affecting the scale of nickel ore supply. According to the Indonesian government's approval in 2024, the total quota is approximately 272 million wmt. As of now, the announced RKAB quota is about 50 million wmt. Due to slow approval progress, subsequent approvals remain uncertain. Under the combined impact of the slow RKAB approval process and the rainy season, nickel ore prices in Indonesia have continued to rise this year. As of the end of May 2025, the CIF price of 1.6% grade nickel ore reached $55 per ton, a 25% increase from the beginning of the year.

According to SMM's forecast, in the short term, nickel ore prices for pyrometallurgy will remain firm. As the previously affected demand for MHP gradually recovers, nickel ore prices for hydrometallurgy may also rise. Throughout the year, the supply-demand dynamics of Indonesia's nickel ore are expected to tighten, with overall prices anticipated to remain high.

Overview of SIMBARA System Application Process

Before the SIMBARA system went live, there might have been tax evasion in some ore sales processes. However, since the SIMBARA system went live in 2025, it has severely cracked down on illegal nickel ore sales, which may have affected the supply of nickel ore in Indonesia's domestic market to some extent.

Over time, mines will gradually complete the required process approvals through the SIMBARA system, and it is expected that the system will gradually become familiar and accepted by local mines and downstream smelters.

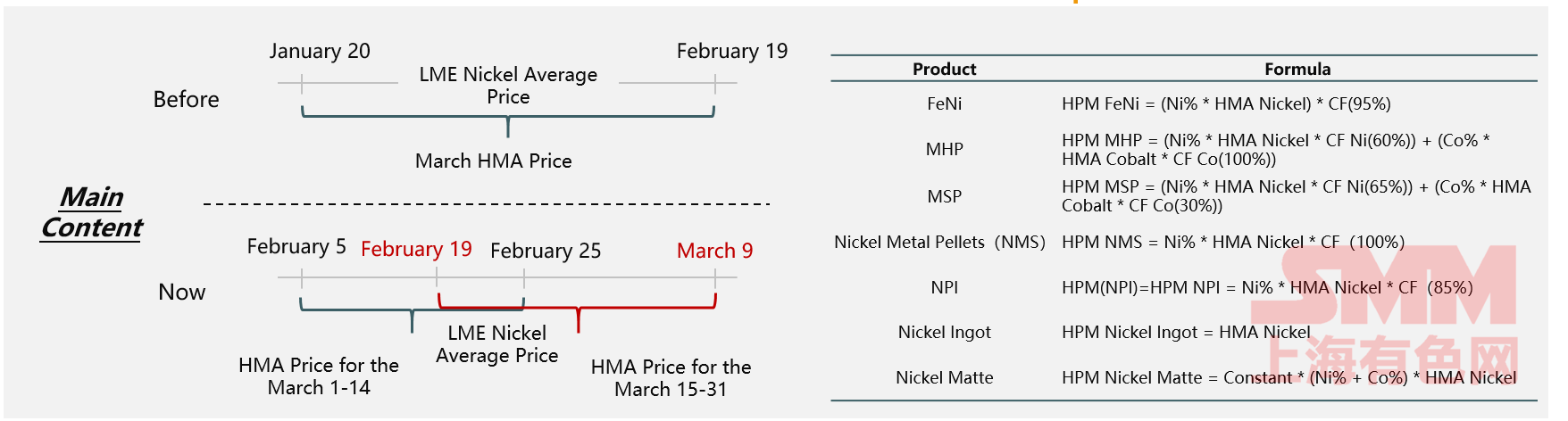

HMA Formula Adjustment and Extension

Nickel Ore:The pricing formula for nickel ore will continue to follow the existing model, with HMA prices adjusted every half-month to more closely track market changes.

Other Nickel Products:The HPM price calculation methods for seven other nickel-based products, excluding nickel ore, have been clarified or newly added to improve pricing transparency and accuracy.

Policy Analysis

Enhancing Market Sensitivity and Pricing Flexibility:More rapidly reflecting the immediate fluctuations in LME nickel prices and reducing pricing lags. Closely linking Indonesia's nickel ore prices with international market prices to avoid price deviations caused by long-term averages.

Optimizing Resource Export Revenue Management:The government can precisely adjust domestic ore prices based on international nickel price fluctuations to safeguard miners' profit margins.

Strengthening Control Over the Nickel Industry Chain:Ensuring the government's comprehensive influence and voice in the nickel industry.

Increasing Fiscal Revenue:Through more accurate value assessments, the government can set more reasonable tax standards, thereby increasing fiscal revenue.

Safeguarding Resource Value:An adjustment mechanism that closely aligns with actual market prices helps stabilize nickel prices and ensures the value of Indonesia's nickel resources.

New Patent Regulations for Nickel Products in Indonesia Officially Took Effect on April 26

On April 11, 2025, the Indonesian President officially signed the new nickel product policy, which took effect on April 26. According to the new regulations, royalties for nickel products will be dynamically adjusted based on the benchmark price (HMA).

The main changes and impacts include:

General Increase in Royalties:The higher the HMA price, the higher the royalty rate.

Strategic Management of Resources Across the Entire Industry Chain:Strengthening strategic management of resources across the entire industry chain.

Enhancing the Value of Raw Materials:Increasing the value of low-value-added raw materials and enhancing the bargaining power of resources.

Hedging Against Price Fluctuations:Reducing risks associated with international market price fluctuations.

Analysis of Indonesia's Imports of Philippine Nickel Ores in 2024

According to SMM, Indonesia imported approximately 10.35 million tons of Philippine nickel ores in 2024. Regionally, Halmahera and Sulawesi accounted for as much as 98% of the nickel ore imports from the Philippines.

Entering 2025, based on current data, Indonesia's nickel ore imports from the Philippines in March increased by 100% compared to the same period in 2024, while in April, they surged by an astonishing 334% YoY.

According to SMM's forecast, Indonesia's total nickel ore imports from the Philippines in 2025 are expected to increase by approximately 45% YoY.

Global Nickel Market's Supply-Demand Balance and Major Trade Flows

Global primary nickel is expected to maintain a supply surplus

SMM predicts that in the short term, influenced by factors such as policies, global nickel supply will tighten, maintaining a tight balance between supply and demand. However, in the long term, the primary nickel market is still expected to face a surplus.

On the supply side, global primary nickel production is expected to maintain a relatively high growth rate in 2025. By segment:

NPI: In 2024, affected by Indonesia's RKAB policy, NPI was in a destocking process last year. In 2025, with the increase in RKAB quotas finalized and the increase in raw material supply, the tight situation of NPI raw materials is expected to be alleviated, leading to an increase in supply. However, considering the combined impact of quota reviews, rainy season effects, and policy uncertainties, the extent of NPI surplus throughout the year is expected to be limited.

Refined Nickel: In 2024, the global primary processing volume was mainly concentrated in the refined nickel sector. In 2025, driven by the expected commissioning of new refined nickel projects in China and Indonesia, global refined nickel capacity will continue to expand, and refined nickel production will significantly increase, further exacerbating the global surplus of refined nickel.

Nickel sulphate: In 2024, amidst slowing downstream demand growth and losses, nickel sulphate enterprises adopted a produce-based-on-sales strategy. Supply and demand maintained a tight balance. In 2025, nickel sulphate enterprises will continue to adopt a produce-based-on-sales strategy, with limited supply growth expected.

Demand side: Downstream stainless steel maintained a steady growth trend; the market space for alloy special steel casting remained relatively limited, with an overall stable growth trend. In the new energy sector, the displacement of ternary lithium batteries by LFP batteries continued, and the growth rate of nickel demand from the new energy sector will further slow down.

Overall, amidst sustained supply growth and slowing demand growth, the fundamental surplus pattern remains unchanged. In the short term, under the macro influences such as tariff policies, sentiment will dominate market trends, with significant fluctuations in nickel prices. In the medium and long term, the supply-demand pattern is still expected to remain in surplus.

Global refined nickel inventory

According to SMM, the surplus issue of global refined nickel remains severe, with the current cumulative inventory reaching approximately 350,000 mt. LME inventory has once again climbed to a high of 200,000 mt. Meanwhile, non-LME registered inventory has also reached approximately 80,000 mt. In the Chinese market, SHFE inventory is approximately 40,000 mt, and social inventory is also approximately 40,000 mt.

In addition, the new refined nickel capacity added this year will continue to be released, with production expected to continue increasing MoM. Therefore, the surplus situation of refined nickel will remain at a high level.

Overview of price spreads and flow changes of major nickel products

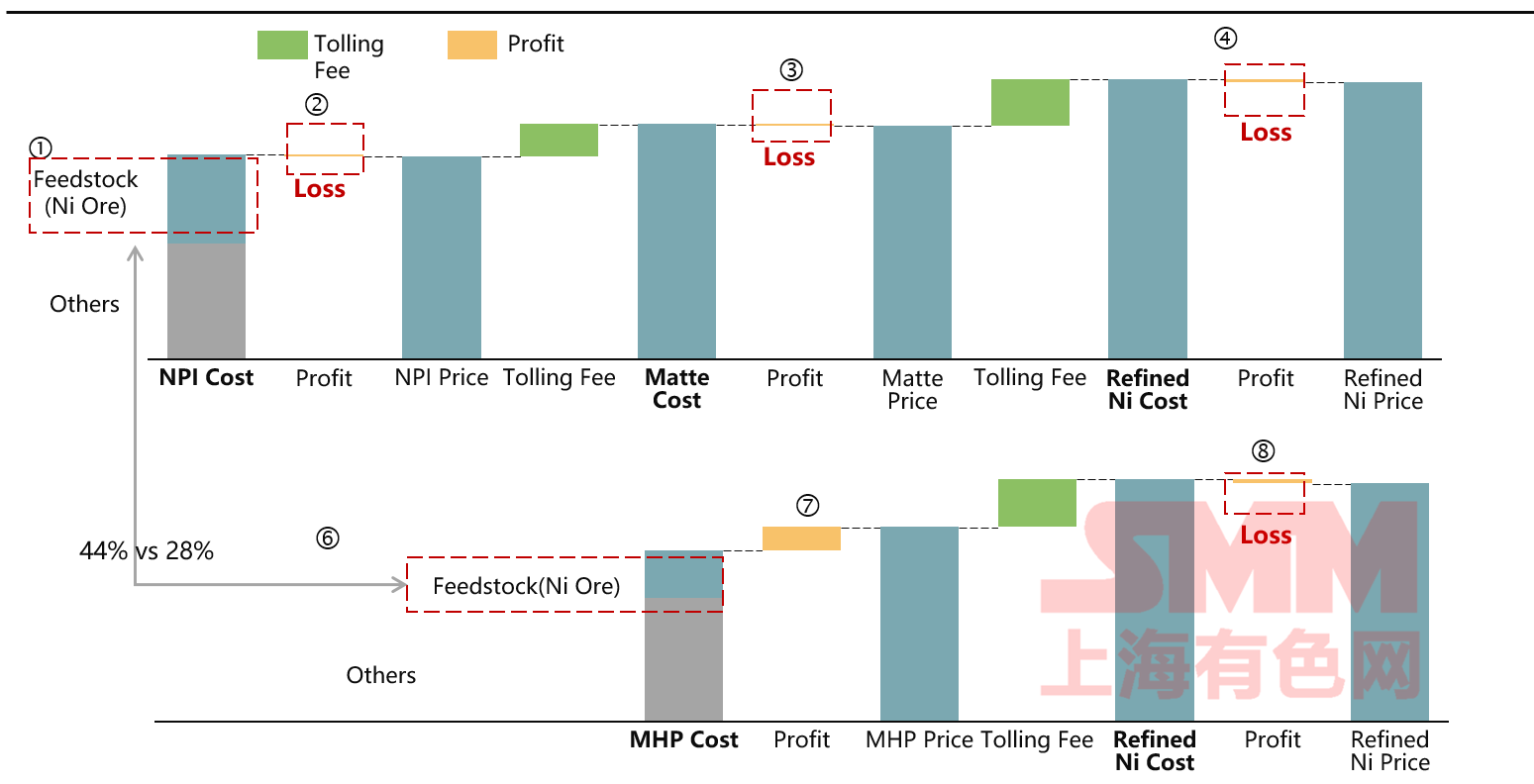

Processing fees and profitability of major nickel products

Let's take a closer look at the current profitability of each specific link in the chain:

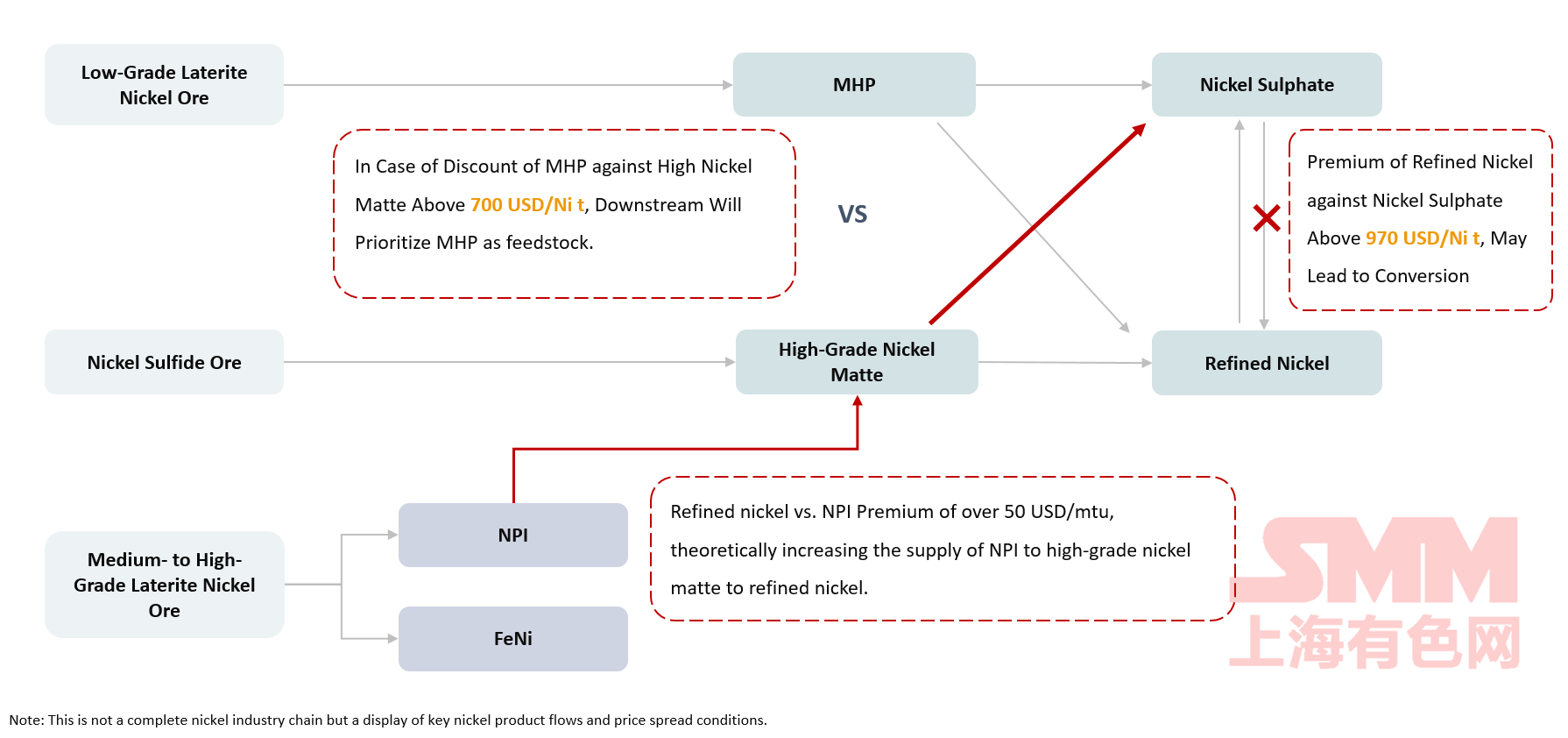

Changes in nickel ore prices will affect the profitability of each link in the industry chain. Since the beginning of this year, as nickel prices have reached a cyclical low, the profitability of each link in the industry chain has been squeezed.

Let's examine the current profitability from the perspectives of pyrometallurgical ore and hydrometallurgical ore smelting paths, respectively.

From the perspective of pyrometallurgical ore, some transformations have occurred in NPI and high-grade nickel matte this year. The processing fee profit from NPI to high-grade nickel matte is approximately $1,800. This year, amidst weak high-grade nickel matte prices and pressure on profits in the high-grade nickel matte link, even leading to partial losses, there has been a significant reduction in high-grade nickel matte production this year. However, the profitability of the NPI link is better than that of the high-grade nickel matte link. Therefore, some production lines that were previously producing high-grade nickel matte have been converted to produce NPI.

Meanwhile, the nickel sulphate link still has slim profits. The refined nickel link, on the other hand, is facing a certain degree of losses.

Global nickel ore and intermediate product trade flows in 2024

Data on trade flows between different countries reflects the respective positions and bargaining power of these countries within the nickel industry chain. After Indonesia banned nickel ore exports, Indonesian nickel products have been exported in the form of intermediate products and further downstream products. China relies on imports for nickel ore and nickel intermediate products. Russia and Australia primarily export nickel ore and intermediate products.

In the NPI segment, Indonesia, with its dual advantages in resources and costs, is a major NPI producer and thus a major NPI exporter.

In terms of refined nickel, global refined nickel trade is closely interconnected. China, Russia, and Indonesia are all major refined nickel sellers. The SHFE in China and the LME in London are both major global refined nickel futures trading markets.

Stainless steel remains the largest source of demand, while the growth rate of new energy has slowed down further.

Downstream demand for primary nickel

Stainless steel is the largest downstream demand sector for primary nickel, accounting for 69% of demand in 2019. However, with the rapid development of the new energy industry, the demand for primary nickel from batteries increased significantly in 2021, leading to a decline in the proportion of stainless steel in primary nickel demand.

Although new energy has entered a relatively stable growth phase, stainless steel is still expected to remain the main consumer sector for primary nickel. It is projected that by 2028, the stainless steel sector will account for approximately 70% of primary nickel consumption.

Nickel, as an important raw material for battery manufacturing, is widely used in fields such as EV batteries and ESS batteries. Due to the rapid expansion of the new energy industry, the demand for nickel in the battery sector shows great potential. However, due to the rising proportion of LFP battery demand, the overall demand for nickel in the new energy sector has increased but has not reached expected levels. It is projected that by 2028, the battery manufacturing sector will account for approximately 11% of nickel demand in the nickel industry.

Indonesia's stainless steel industry has grown rapidly due to its strong cost competitiveness and abundant resources, with significant future growth potential.

As a major source of demand for nickel, stainless steel is mainly supplied by China. However, the increase in Indonesia's stainless steel supply in the future will also be worth noting. Indonesia mainly produces 300-series stainless steel. In 2024, stainless steel production was approximately 480,000 mt. In the future, Indonesia will continue to increase its supply at a compound annual growth rate of approximately 5.9%.

Indonesia's stainless steel exports

Indonesia currently mainly exports 300-series stainless steel, with its main markets concentrated in Asia. In 2024, Indonesia exported a total of 4.75 million mt of stainless steel, of which 1.57 million mt was exported to mainland China, accounting for 33% of total exports.

China mainly imports 2E-grade stainless steel and cold-rolled stainless steel from Indonesia. After imported stainless steel enters China, it undergoes further processing by Chinese enterprises, such as bright surface finishing (matte treatment), transforming it into products with a smooth and even surface before being sold.

It should be noted that Indonesia's stainless steel export data may not fully align with its actual production. Reasons for this discrepancy include:

1. Inventory impacts due to delayed export timelines;

2. Indonesia's stainless steel imports;

3. Unaccounted-for capacity of approximately 200,000 mt from small local enterprises in India.

Battery Demand Dynamics: Decline in NCM Market Share, Medium-to-High Nickel to Become Mainstream

SMM forecasts that from 2025 to 2027, the market share of NCM lithium batteries will continue to decline, with medium-to-high nickel batteries potentially becoming the mainstream of future NCM lithium batteries.

The increasing proportion of 8-series and 9-series high-nickel NCM lithium batteries has led to an increased demand for nickel.

All-Solid-State Lithium-Ion Batteries in Early Development Stage

As a highly anticipated future field, solid-state batteries are viewed by many as another significant potential growth point for nickel applications. However, from the current stage of development, solid-state batteries are still in the early exploration phase. Currently, issues such as high costs, unstable material systems, and low energy density need to be addressed.

The future development of solid-state batteries can be divided into three main stages. Firstly, from now until 2027, we anticipate that solid-state batteries will achieve a breakthrough from 0 to 1. In this stage, the cathode material will adopt a high-nickel NCM system, while the anode will utilize a low-silicon doping scheme. However, cost and energy density will remain critical issues to overcome.

Entering the second stage, from 2027 to 2030, we expect the energy density of solid-state batteries to exceed 400, with costs significantly reduced, enabling gradual large-scale application.

In the third stage, from 2030 to 2035, solid-state batteries are projected to enter the commercial application phase, with energy density exceeding 500. In this stage, solid-state batteries will bring substantial growth in nickel demand.

》Click to view the special report on the 2025 Indonesia Mining Conference & Critical Metals Conference

![This Week, Platinum and Palladium Experienced Significant Pullbacks, End-Use Demand Recovered, and Spot Market Trading Was Normal [SMM Platinum and Palladium Weekly Review]](https://imgqn.smm.cn/usercenter/obeMy20251217171735.jpg)

![Silver Prices Continue to Pull Back, Suppliers Remain Reluctant to Sell, Spot Market Premiums Hard to Decline [SMM Daily Review]](https://imgqn.smm.cn/usercenter/LVqfJ20251217171736.jpg)